Many governments and corporations have made bold commitments to tackle climate change, labelling the next 10 years as the “decade to deliver”. Technology lies at the heart of those attempts to prevent, or even reverse, global warming. Intelligent products, new applications of existing technology or even entirely new business models are emerging to increase energy efficiency, reduce overall energy consumption or expand the use of renewable energies.

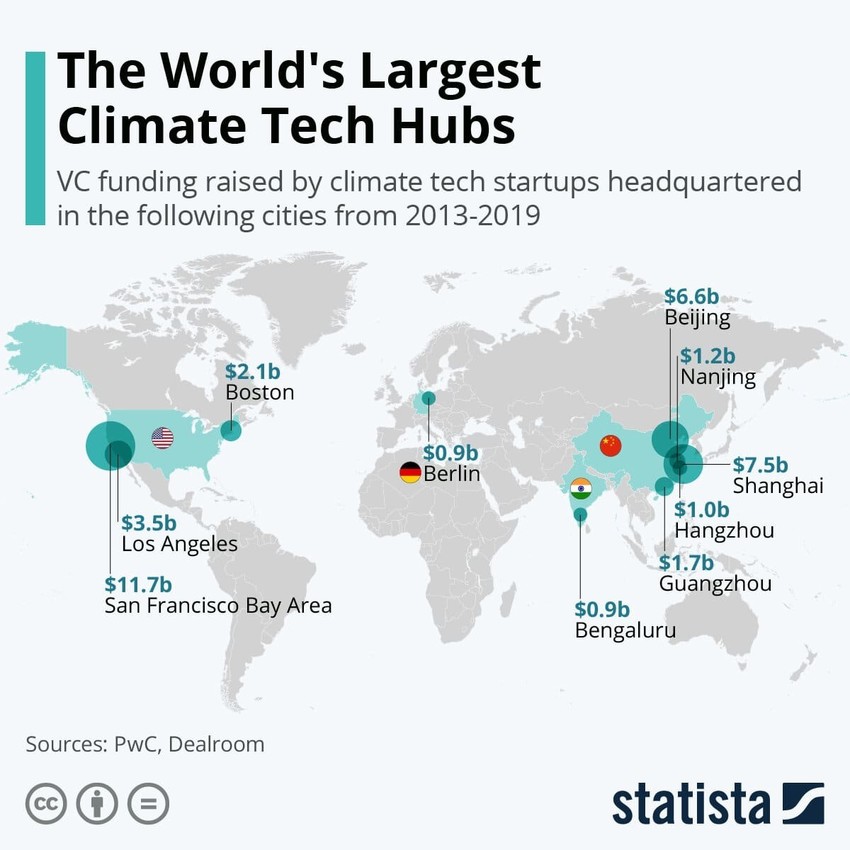

More than 1,200 so-called “climate tech” start-ups have already been identified. Switzerland, the Global Innovation Index leader since 2011, is one country providing fertile ground for ventures tackling climate change. Together with more established players, these start-ups will be crucial in unlocking major investment opportunities for corporations and investors.

Channelling these investments is a critical challenge for the global financial system. Investors representing more than $45 trillion in assets under management have already agreed to drive climate change action across their portfolios. Sustainable finance has, therefore, become an integral part of how many financial services firms operate. We strongly believe that sustainable finance, combined with technological innovation and digitalization in banking, will be instrumental to sustainable innovation and growth and the transition to a less carbon-intensive economy.

What is sustainable digital finance?

Digital finance refers to the integration of big data, artificial intelligence (AI), mobile platforms, blockchain and the Internet of things (IoT) in the provision of financial services.

Sustainable finance, on the other hand, refers to financial services integrating environmental, social and governance (ESG) criteria into the business or investment decisions for the lasting benefit of both clients and society at large.

Combined, sustainable digital finance is increasingly demonstrating its ability to address barriers and promote sustainable economic growth.

It is added sugars that have been cited as a contributor to many health problems. In December 2014, MNT reported on a study in the journal Open Heart claiming added sugars may increase the risk of high blood pressure, even more so than sodium. And in February 2014, a study led by the Centers for Disease Control and Prevention (CDC) associated high added sugar intake with increased risk of death from cardiovascular disease (CVD).

Enabling sustainable investment choices

Access to high-quality and comparable data will be vital to increase opportunities for more sustainable investments. Data is the backbone of investment decision-making: investors need help to understand how companies may fare as the environment changes, regulation evolves, new technologies emerge and customer behaviours shift. They need to better understand and quantify risk as well as returns. Increasingly, investors are looking for ways to measure the impact of their portfolios and set benchmarks.

As a consequence, the ESG data market is booming. Data providers have developed a full gamut of ESG products ranging from raw data to aggregated scores, and have multiplied their data sources. With an expected annual growth rate of 20% for ESG data and 35% for ESG indices, the overall market could approach $1 billion by 2021.

To compare and discern meaningful information will be increasingly challenging for investors owing to:

- a lack of certain data e.g. indirect carbon emissions in the value chain of a company;

- an absence of standards and consistent regulation;

- the sheer volume of data.

By 2025, estimates indicate that there could be more than 160 zettabytes of data in the world and that 80% of this data will be unstructured. Going forward, it is widely expected that technologies like AI, machine learning and natural language processing will be used to both generate and evaluate ESG data. These technologies can help process vast amounts of data, including in sectors where information is often presented in incompatible ways. They will also effectively ascertain signals embedded in unstructured data to gain deeper or even predictive insights into sustainable investment. These technologies will also make it possible to reduce the costs of searching for information and improve the measurement and tracking of the “greenness” of investments.

Technology is, however, not a panacea, but an effective way of strengthening human judgement and amplifying the effectiveness of ESG analysis. The availability of high-quality, data-driven insights will assist financial institutions in improving the sustainability profile of investor portfolios and in advising clients on how to align investments to their individual preferences.

Financial institutions can also create innovative financing models that steer client money to promising new projects and cutting-edge start-ups. For climate aware investors, modelling the potential financial impact of climate change on specific assets or portfolios can help them understand their climate risk exposure. Equipped with this information, investors might then consider how to mitigate, adapt or transition their portfolios.

- Portfolio mitigation: lowering investment exposures to carbon risks (step-by-step);

- Portfolio adaptation: increasing investment exposures to climate-related solutions, assets more resilient to the effects of climate change or into technologies that combat it;

- Portfolio transition: aligning investments to and making sure they are on track with the chosen climate pathway (whether that is a 2°C world, a 1.5°C world or a different trajectory altogether).

Incentivizing sustainable consumer choices

In addition to powering investment decisions, technology can also help raise consumer awareness about the environmental and social implications of consumption and investment decisions, and incentivize them to more resource-efficient and sustainable choices.

The consumer FinTech industry is in the midst of staggering growth in global adoption, from 16% in 2015 to 64% in 2019. The widespread use of mobile and e-banking applications opens new opportunities for financial institutions to provide transparency to consumers about their daily consumption patterns and support them in selecting products and services that align to their personal values.

Take big data and AI as an example: these can be used to translate financial transaction data into individual carbon footprints, which when integrated with digital banking services, make it possible to highlight the environmental impact of purchases in real time. More aware consumers who increasingly buy environmentally friendly products and services will in turn incentivize investments into greener production.

Responding to consumer demands will benefit the environment as well as business. Companies focusing on sustainability can expect to become increasingly attractive to investors, as outlined earlier. Furthermore, research shows that more than 50% of consumers are willing to pay more for sustainable products designed to be reused or recycled. In Switzerland, 42% of millennials started or deepened a business relationship because of a company’s positive impact on society or the environment.

Sustainable products are starting to demonstrate higher growth rates than their non-sustainable rivals. In the US, sustainability-marketed products make up just 16% of the consumer packaged goods market, but are responsible for 55% of the growth. The products also enjoy a hefty premium and continue to grow faster than their conventional counterparts.

Transitioning into a sustainable, low-carbon economy

Private investment as well as consumer choices will be critical to tackling climate change and will play an important role in closing the climate finance gap. The increased awareness of climate-related economic benefits and risks in the wake of COVID-19 has further focused investors on environment-related opportunities.

Before the pandemic, Carbon Tracker, an independent financial think tank, calculated that the renewable energy investment opportunity alone could reach $1 trillion per annum. It is also estimated that jobs in renewables could reach 42 million globally by 2050, four times their current level. With the integration of renewable energy, smart buildings and greener public transport into economic stimulus packages following the pandemic, this opportunity is expected to increase even further.

We believe that sustainable digital finance will play an essential role in efficiently channeling this capital to fuel innovation, growth and job creation, at the same time supporting the transition to a sustainable, low-carbon economy.

Karin Oertli, Chief Operating Officer, Personal and Corporate Banking and Switzerland, UBS